J.B. Broekaert, et al. Cognitive Psychology 117 (2020) 101262

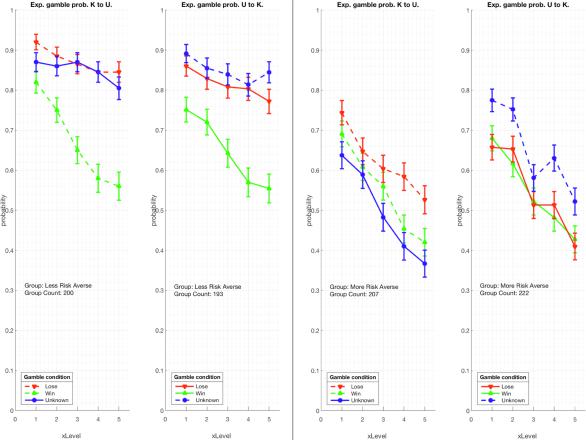

From Fig. S3, we observe that a substantial fraction of the participants obtained a single-gamble score of 10. Participants that always take the initial gamble, regardless the payoff, can be considered more risk-seeking than participants that will not always take it. This criterion warrants a partitioning of the sample by either obtaining a single-gamble score less than 10 or the maximum of 10, resulting in a ‘More risk averse’ group (N = 429) and a ‘Less risk averse’ group (N = 393) which are approximately of the same size.7 A first overall observation of the second-stage gamble probabilities separated along our criterion for risk attitude, Fig. 4 confirms some basic expectations. The defined ‘More risk averse’ group is indeed more risk averse than the defined ‘Less risk averse’ group, since all gamble probabilities for all payoff values X and for all outcome conditions are lower in the ‘More risk averse’ group in comparison to the same gambles taken by the ‘Less risk averse’ group. Moreover, the ‘More risk averse’ participants have a faster diminishing motivation to take the second-stage gamble for increasing payoff X when the first-stage gamble outcome was Lose or Unknown. However, when the first-stage gamble outcome was Win, this diminishing motivation to gamble over X remains the same for both groups. The ‘Less risk averse’ participants also show a significant distinction between gamble choices under W and L condition, while the ‘More risk averse’ participants hardly discriminate between these two conditions.8

A major and rather surprising observation for the ‘More risk averse’ group is the strong flow-order with outcome-condition crossover interaction (Fig. 4, right panel). Remarkably the ‘More risk averse’ participants show a tendency for a Disjunction Effect in K-to- U order and a significant inflative violation of the LTP in U-to-K order. Notice that this is a between-participants effect of flow order. A mixed ANOVA with unbalanced design (N = 207/N = 222) and with a dependent variable gamble probabilities (averaged across all payoffs X) and independent variables first-stage gamble outcome condition {W, L, U} and order {‘K-to-U’, ‘U-to-K’} revealed a significant interaction, F (2, 1281) = 12.78, p = 3. 20e  06 .

06 .

By contrast, there were no main effects for either first-gamble outcome condition or order in the ‘More risk averse’ group. That is, surprisingly, there appears to be no effect on choice behavior from whether the first-stage gamble was indicated as Won or Lost.

The ‘Less risk averse’ participants do not show any tendency for a Disjunction Effect in the order K-to-U, while in the U-to-K order a non-significant tendency for an inflative violation of the LTP occurs. A mixed ANOVA with unbalanced design (N = 200/N = 193), testing for factors of condition {W, L, U} and order {‘K-to-U’, ‘U-to-K’}, revealed a significant main effect of condition {W, L, U} F (2, 1173) = 43.88, p = 4. 2e  19 . Therefore, in this group a substantial difference in gambling probability is observed, depending on whether the first-stage gamble was Won or Lost.

19 . Therefore, in this group a substantial difference in gambling probability is observed, depending on whether the first-stage gamble was Won or Lost.

In the U-to-K order the ‘More risk averse’ participants are mostly indifferent to choice under the Win or Lose first-stage gamble outcome condition, therefore the inflative violation of the LTP has to be tested with respect to both choices of the two Known outcome conditions. To test the statistical significance of the violation of the LTP the Wilcoxon test for repeated measurements on a single sample was applied. The test was used to assess the paired difference from measurements on Known and Unknown conditions for each participant. The Wilcoxon test shows a significant violation of the LTP, with p = 1.7e-06 (N = 222) for H0 that

p(g|U, X ) X < p (g|L, X ) X and p = .0002 (N = 222), for H0 that p(g|U, X ) X < p (g|W , X ) X .

In the K-to-U order the ‘More risk averse’ participants show a small but consistent diminished choice probability under Win in comparison to the Lose first-stage gamble outcome condition. In this case therefore the Disjunction Effect is tested between the choices in the Unknown and Win outcome conditions only. The Wilcoxon test shows a significant Disjunction Effect, with p = .045

(N = 207), for H0 that p(g|U, X ) X > p (g|W , X ) X . Since this result seems marginally significant, we also applied the Pratt correction to the Wilcoxon test (by modification of Matlab code in Cardillo (2006)). The Pratt correction is required for samples with frequent ties, which typically occur in discrete distributions like in our present data set where the compared X-averaged gamble response values are fractions ranging from 0/5 till 5/5. While the Wilcoxon test eliminates all zero differences of measurement outcomes, the Pratt correction keeps the zero differences in the ranking procedure of the statistical test (Pratt, 1959). Using the Pratt correction, the Disjunction Effect for ‘More risk averse’ participants in the K-to-U order is marginally not statistically significant anymore at p = .062 (N = 207).

The size of the sample allows insight in decision patterns besides aggregate gamble probability. In particular we can consider the prevalence of particular gamble strategies expressed as WLU gamble patterns, Fig. 5. Three gamble patterns have a deflative effect on the average gamble probability under Unknown condition –(g|W , s|L, s|U), (s|W, g|L, s|U ) and (g|W , g|L, s|U)– and three have an inflative effect – (g|W , s|L, g|U), (s|W, g|L, g|U) and (s|W , s|L, g|U), Table S1. The probability distribution over the patterns causes the occurrence of either a Disjunction Effect or an inflative violation of the Law of Total Probability. It is therefore important to analyse the distribution of the gamble patterns over the spectrum of payoff parameter X, Fig. 5.

A remarkable difference between the pattern distribution of the ‘Less risk averse’ and ‘More risk averse’ participants occurs over the range of increasing payoff X. In ‘Less risk averse’ participants the modal strategy remains ‘always play’, (g|W , g|L, g|U ), throughout the X range. In the ‘More risk averse’ participants the modal pattern changes from ‘always play’ at the lowest payoff to ‘never play’, or (s|W , s|L, s|U), at the highest payoff.

7 The demographics for the ‘Less risk averse’ group with respectively NKU = 200 and NUK = 193 participants revealed respective gender means

mgender = 0.61 and mgender = 0.52, while the ‘More risk averse’ group had NKU = 207 and NUK = 222 participants, with respective gender means

mgender = 0.48 and mgender = 0.46. Therefore a small gender bias was present due to our risk-aversion partitioning, (p = .006, two-tailed) where the |

odds ratio is 0.68 and the confidence interval CI = [0.52, 0.89] for |

= |

.05 |

. |

8 |

|

|

|

In SM 10, we analyse the effect of informing the participant about the Unknown outcome of the first-stage in a two-stage gamble by comparing |

the probability of taking the single-stage gamble p(g) (thus without any condition set by an earlier stage gamble) and the second-stage gamble p(g|U ) (in which the participant is informed that the outcome is Unknown). This analysis is done for ‘more risk averse’ participants, since for ‘less risk averse’ participants p(g) = 1 for all X, hence further analysis is not pertinent for the latter participant group.

[1, 5] appears on the x-axis. Error bars represent the standard error of the mean.

[1, 5] appears on the x-axis. Error bars represent the standard error of the mean.

. The probability for the participant to take the second-stage gamble is obtained by adding the two components ‘Gamble in the second-stage and Won-first- stage belief’ and ‘Gamble in the second-stage and Lost-first-stage belief’

. The probability for the participant to take the second-stage gamble is obtained by adding the two components ‘Gamble in the second-stage and Won-first- stage belief’ and ‘Gamble in the second-stage and Lost-first-stage belief’